Australia’s rate outlook has shifted again as Iran-conflict disruptions push energy and import costs back into inflation models. The rate debate shifted on March 12, 2026

Rate Relief Starts to Reverse

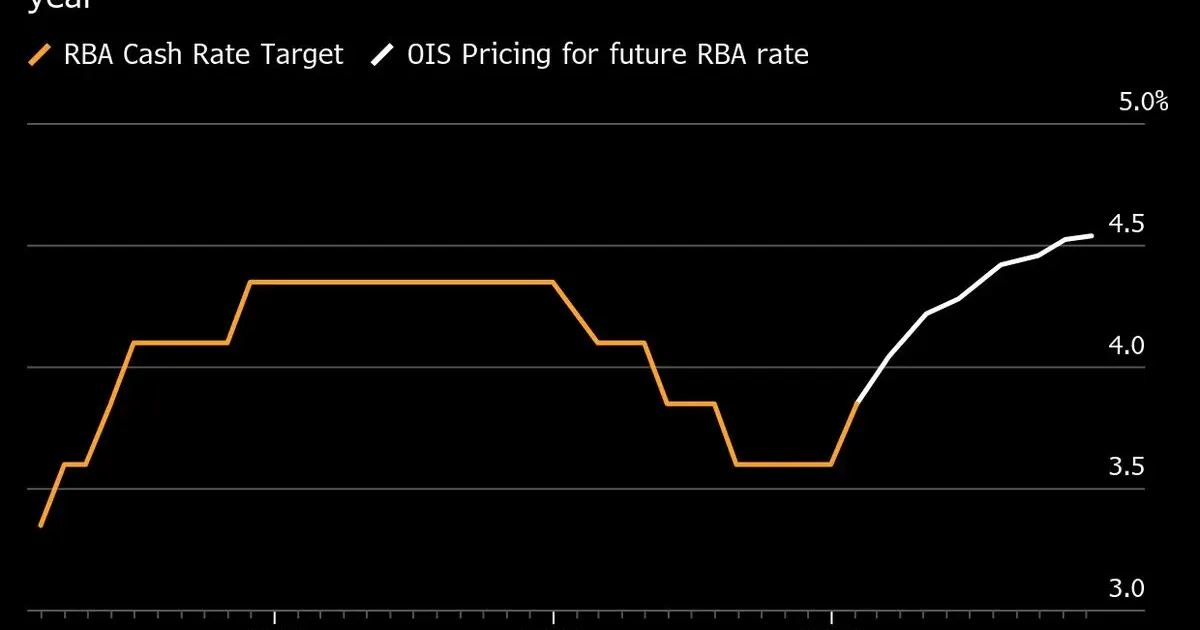

The rate outlook marks a harsh realization for policymakers in Sydney. Reserve Bank of Australia officials are preparing to dismantle the entire framework of monetary relief established only months ago. Military escalation in the Middle East has shattered the fragile stability of global energy markets, forcing the central bank into a defensive posture. Traders and economists now anticipate a swift return to restrictive policy as the ghost of inflation returns to haunt the domestic economy. Investors spent the majority of 2025 celebrating a sequence of rate cuts that many hoped would signal a permanent end to the cost-of-living crisis. Those reductions were categorized by analysts as short and shallow, a cautious attempt to breathe life into a cooling housing market. That optimism has vanished. Current market pricing suggests a minimum of two 25-basis-point increases are imminent, effectively erasing every gain made by mortgage holders during the previous year's easing cycle. Central bank leadership finds itself in an unenviable position. While Bloomberg Economics points to a consensus among institutional forecasters that tightening is inevitable, the speed of the shift has left retail banks scrambling to adjust their own lending projections. Rising price pressures have proven far more resilient than the models predicted. The conflict in Iran acted as the catalyst, turning a manageable inflationary breeze into a gale-force wind that threatens to blow the RBA off its target path. War remains the ultimate disruptor of financial models.

Energy Shock Reaches the RBA

Energy shocks from the Iran conflict changed Australia's inflation outlook. Petroleum prices sit at the heart of this sudden economic redirection. Because Australia relies heavily on imported refined fuels, the maritime instability surrounding Iranian shipping lanes has a direct, immediate impact on the pump. Crude oil surged past 110 dollars per barrel last week, a price point that creates a domino effect across the entire supply chain. Groceries, construction materials, and consumer electronics all carry a hidden fuel surcharge that is now being passed directly to the public. Supply chain logistics are buckling under the pressure of increased insurance premiums and rerouted tankers. Shipping companies have largely abandoned the most direct routes, opting for longer, more expensive journeys to avoid the combat zone. These added costs do not simply disappear; they embed themselves in the consumer price index. Economic data released on Tuesday showed that transport-related inflation reached a three-year high, prompting immediate concern inside the Reserve Bank's boardroom. Financial analysts at major Sydney firms have spent the last 48 hours revising their terminal rate forecasts. The suddenness of the Iranian escalation caught many off guard, as the previous narrative focused on a soft landing for the Australian economy. Instead of a soft landing, the RBA now faces a potential stall. High energy costs act like a tax on every household, draining discretionary income and slowing down the retail sector even as interest rates climb. Domestic price pressures are no longer confined to the energy sector.

Households Face Another Squeeze

Services inflation, which had shown signs of moderating in late 2025, has re-accelerated as businesses anticipate higher operating costs for the winter. Rent remains a persistent pain point for millions of Australians, and the prospect of higher interest rates provides little comfort to those hoping for a reprieve. Property values have slowed their ascent, but the cost of servicing existing debt is about to become sharply more burdensome. Reserve Bank Governor Michele Bullock has signaled that the board will not hesitate to act if price stability is threatened. This policy u-turn reflects a global trend where central banks are being forced to prioritize currency defense over domestic growth. As the US Federal Reserve maintains a hawkish tone to combat its own geopolitical headwinds, the Australian dollar has come under intense selling pressure. A weaker dollar makes imports even more expensive, creating a vicious cycle of imported inflation that only higher domestic rates can break. This newfound aggression from the central bank is a warning to those who believed the era of high rates was a historical anomaly.

Cheap credit has disappeared again. Households that had only just begun to find their footing after the 2023-2024 tightening cycle must now prepare for a renewed squeeze on their monthly budgets. The math for many families simply no longer adds up. Quantitative analysts are currently dissecting the Bloomberg data to determine exactly how high the RBA might go.

While the initial forecast calls for two hikes, some more pessimistic observers suggest a third increase could be necessary if the Iran conflict extends into the second half of the year.

Imported Inflation Narrows the Options

The primary concern is the potential for a wage-price spiral. If workers begin demanding higher pay to cover their increased fuel and grocery bills, the RBA may be forced to push the economy into a deliberate recession to kill off demand. Historical parallels are being drawn to the energy shocks of the late 1970s, where geopolitical instability in the same region led to a decade of stagnant growth and high inflation. Modern central banking is supposed to be more sophisticated, yet the fundamental reliance on stable energy prices remains a glaring vulnerability.

Australia's transition to renewable energy is underway, but it is not happening fast enough to insulate the currency or the consumer from the immediate fallout of a Middle Eastern war. Economic growth projections for the 2026-2027 fiscal year are being slashed across the board. Real estate developers have already begun pausing new projects, citing the uncertainty of future borrowing costs. This reduction in housing supply will likely keep rents high, even as the broader economy slows.

It is a paradox that leaves the central bank with very few good options. Stability has vanished.

The Soft Landing Was Too Fragile

Australia prepared for possible interest rate hikes after Iran conflict disruptions lifted inflation risk. Higher oil, shipping and import costs threatened to reverse the previous easing cycle. A weaker Australian dollar can worsen imported inflation and pressure the RBA to act. Households with mortgages face renewed stress if rate relief is reversed.

A Middle East conflict can affect Australian rates because energy and shipping shocks can raise inflation, weaken the currency and force the central bank to tighten policy. Mortgage holders, renters, import-reliant businesses and low-savings households are especially vulnerable.

The lesson is blunt: an easing cycle built on calm energy markets can vanish when the oil shock returns. The RBA may not control the war, but it controls whether inflation expectations are allowed to drift. Households will pay the price for a global shock they did not cause.