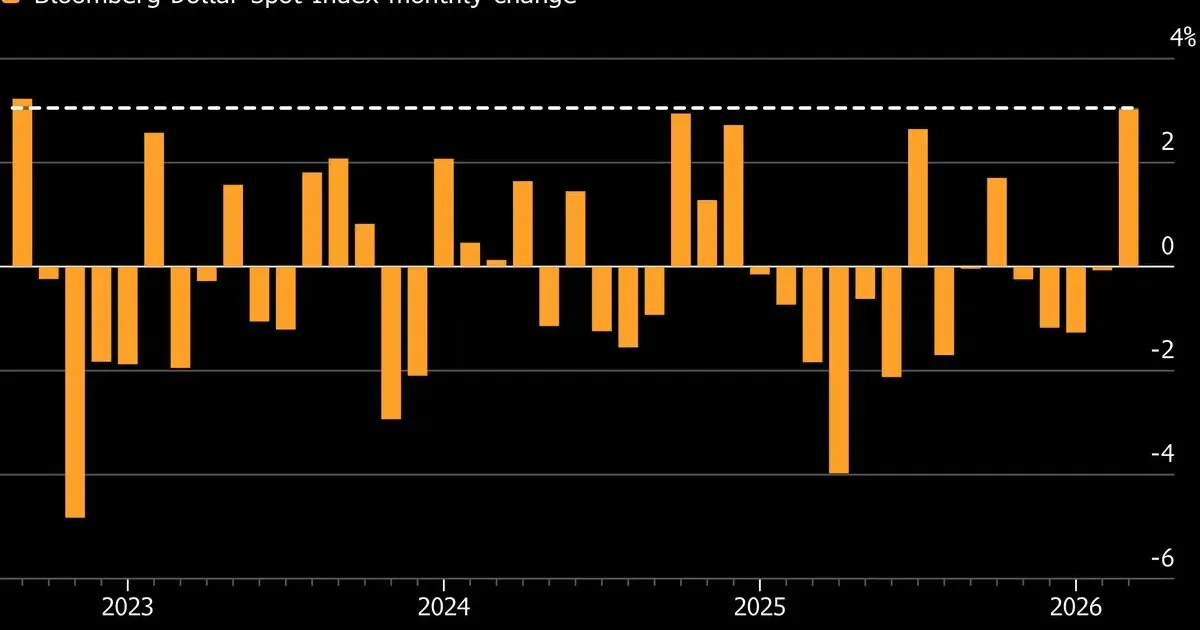

This flight to safety propelled the US Dollar to its strongest monthly performance since October 2024. Markets in London and New York are now pricing in a sustained period of high energy costs and currency volatility. Capital flows shifted rapidly throughout the final trading sessions of the month, favoring the world's primary reserve currency over emerging market assets and European equities.

Geopolitical instability involving Iran triggered a re-evaluation of global growth forecasts for the remainder of the fiscal year. Currency traders noted that the greenback outperformed all other G10 currencies as the risk of a broader regional conflict increased. While some analysts initially expected a cooling of inflationary pressures, the sudden disruption of shipping lanes through the Strait of Hormuz changed those calculations. Energy futures spiked during the early morning hours, forcing hedge funds to liquidate short positions in favor of dollar-denominated cash reserves.

Energy Markets Disrupt Global Reserve Dynamics

Oil prices surged toward triple digits, creating an immediate inflationary headwind for major economies. Brent crude rose by 4.2 percent in a single session, reflecting fears that energy infrastructure could become a primary target in the escalating hostilities. High energy costs typically strengthen the dollar by increasing the demand for currency required to settle international fuel contracts. This correlation intensified as news of a military strike on a major refinery complex reached the trading floors of the Singapore Exchange.

Bloomberg reported that the US Dollar index is on track to finalize its most meaningful monthly gain in nearly two years. Supply chains, already strained by logistical bottlenecks, now face the prospect of a long-term closure of Mediterranean transit routes. Market participants often view the American currency as the only viable shelter during periods of extreme military uncertainty. Central banks in Asia intervened in the overnight markets to support their local currencies, though these efforts provided only temporary relief against the relentless dollar rally.

Equity markets experienced broad sell-offs in the technology and industrial sectors, which are particularly sensitive to rising input costs. Corporate earnings calls for the first-quarter of 2026 have been dominated by discussions regarding fuel surcharges and currency hedging strategies. Large-cap exporters in Germany and Japan are seeing their profit margins eroded by the combined pressure of high energy prices and a surging dollar. Investors believe the current trend will persist as long as the diplomatic path toward a ceasefire remains blocked by hardline rhetoric on both sides.

Nationwide Forecasts UK Housing Market Softening

Across the Atlantic, the British property sector began to show signs of strain according to the latest data from Nationwide Building Society. Lending officers noted that the market initially regained momentum during the early weeks of March. However, the surge in energy costs and the resulting pressure on disposable income began to dampen buyer enthusiasm by month-end. Mortgage rates, which had stabilized in February, are creeping upward again as the Bank of England considers how to combat the inflationary impact of the Iran war.

Nationwide analysts emphasized that consumer confidence is highly sensitive to external shocks. Prospective buyers are increasingly cautious about committing to long-term debt when utility bills are projected to rise by 15 percent by the summer. Real estate agents in the Southeast of England reported a decrease in new property listings, suggesting that homeowners are choosing to stay put rather than risk a move in an unstable economic environment. Lenders are tightening their affordability criteria to account for the rising cost of living, which effectively reduces the maximum borrowing capacity for most households.

Nationwide reported that while the market regained momentum in March, rising mortgage and energy costs could hit consumer confidence.

Robert Gardner, chief economist at Nationwide, pointed out that the housing market has historically lagged behind changes in the broader macro environment. Current trends suggest that the modest price growth seen in the early part of the year may be wiped out by a summer stagnation. Data from the lender showed that the average UK house price rose by 1.6 percent year-on-year in March, but month-on-month figures were flat. This slowdown indicates that the tailwinds from a potential interest rate cut have been neutralized by the geopolitical crisis.

Central Banks Face Inflationary Energy Shocks

Federal Reserve officials in Washington are monitoring the dollar's appreciation with cautious interest. A strong currency helps to lower the cost of imports, which can act as a natural brake on domestic inflation. By contrast, it hurts American manufacturers who find their products more expensive in foreign markets. The central bank faces a difficult balancing act, needing to maintain high enough interest rates to curb energy-led inflation without causing a deep recession. Recent speeches by Fed governors suggest that the planned rate cuts for 2026 may be postponed indefinitely.

Eurozone policymakers are in a more unstable position given their closer proximity to the conflict zone and higher dependence on imported energy. The euro fell to its lowest point against the dollar in eighteen months as investors grew skeptical of the European Central Bank's ability to stimulate growth. Industrial output in the Rhine Valley has already begun to contract, leading to fears of stagflation across the continent. Military developments in the Middle East are now the primary driver of monetary policy decisions in Frankfurt and London alike.

Gold prices, usually a hedge against inflation, have performed inconsistently. While bullion initially spiked at the start of the Iran war, the extreme strength of the Dollar has capped its upside potential. Many institutional investors are choosing the yield-bearing safety of US Treasuries over non-yielding gold bars. The behavior highlights the dominance of the American financial system during times of global duress. Capital continues to seek the most liquid and secure destination as the world enters a period of deep uncertainty.

Emerging markets are the most exposed because the same move raises dollar debt costs and import bills. That combination can force governments to defend currencies at the expense of domestic growth.

Dollar Haven Demand

The dollar rally is a safety trade with consequences. A stronger dollar can calm some investors while tightening financial conditions for countries that borrow, import fuel or defend weaker currencies.