Moody's Investors Service issued a formal warning about the deteriorating fiscal trajectory of France as political paralysis takes hold in Paris. Financial analysts at the agency noted that while the current credit assessment remains at Aa3, the window for meaningful deficit reduction is closing. Failure to implement structural reforms could push the debt-to-GDP ratio permanently higher.

By April 12, 2026, recent data showed the national budget gap widening beyond previous projections and leaving the government with little room for error. Economic stability in the eurozone depends heavily on French fiscal discipline. Internal agency documents suggest that the inability of the European Union to enforce its latest spending rules has emboldened various factions within the National Assembly to prioritize local interests over macro-financial health. Revenue growth has slowed sharply compared to the early decade peaks. Tax collections from corporate profits fell short of targets in the first quarter of the year. Spending on social programs continues to rise without corresponding funding mechanisms.

Moody's Maintains Rating Despite Fiscal Deterioration

Maintenance of the Aa3 rating is a temporary reprieve for the administration of Emmanuel Macron. Investors typically view this specific grade as high quality, yet the accompanying commentary from the rating agency was unusually blunt. Credit analysts pointed to the persistent gap between government spending and tax receipts. Current estimates place the primary deficit at levels that would have triggered immediate sanctions under previous regulatory regimes. The stability outlook rests on the assumption that the government will eventually find a path to consolidation.

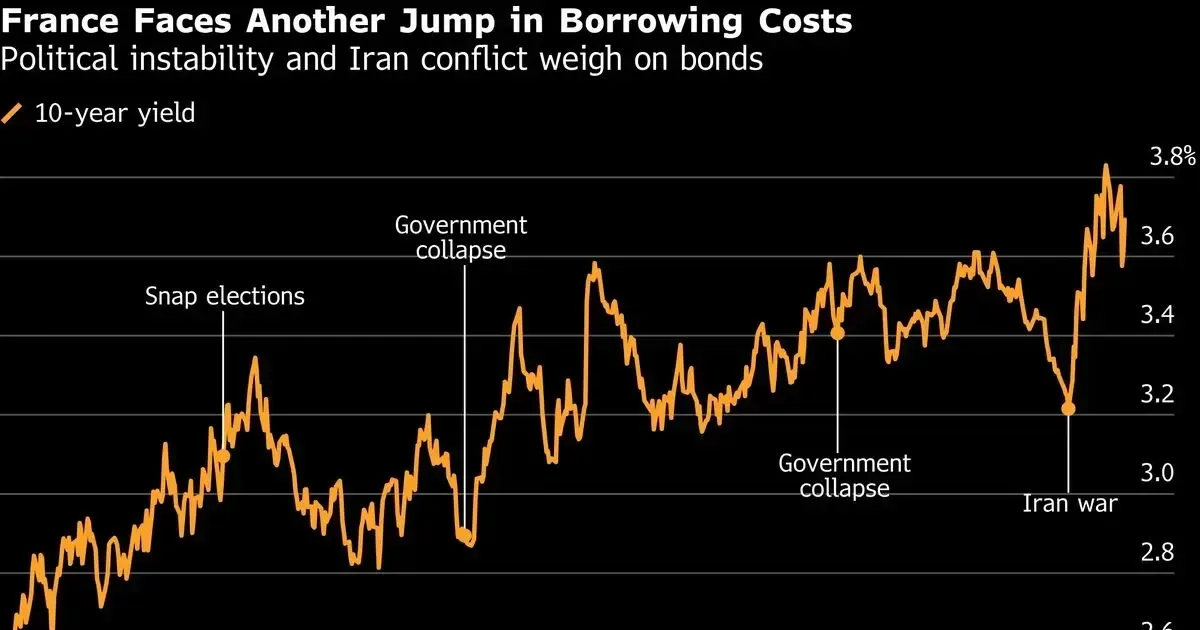

Debt servicing costs for the French Treasury have climbed steadily over the past eighteen months. Yields on ten-year OATs, the benchmark for French sovereign debt, recently moved upward as the market processed the latest ratings report. Borrowing costs now sit at their highest levels since the peak of the global inflation surge. Fiscal hawks in the ministry of finance express private concern that the era of cheap debt has ended permanently. They worry that interest payments will eventually crowd out essential public investments in technology and infrastructure.

Moody's Ratings warned that France's political divisions and the buildup to presidential elections risk thwarting further efforts to reduce the bloated deficit even as it maintained its Aa3 assessment of the country. Public debt in the second largest economy of the euro area surpassed $3.2 trillion recently. Managing such an enormous portfolio requires constant market confidence which is currently under threat. Rating agencies look for a credible medium-term plan to bring the deficit under the 3% ceiling mandated by regional treaties. French officials have missed these targets consistently over the last four cycles. Each missed milestone erodes the credibility of the national treasury in the eyes of international bondholders.

Political Polarization Paralyzes French Budget Reform

Political factions in the National Assembly have reached a total deadlock regarding the 2027 fiscal plan. No single party holds a majority, meaning every euro of spending requires a compromise that usually results in more debt rather than less. The European Union has watched with increasing frustration as Paris avoids the difficult choices necessary to stabilize its books. Legislative gridlock has effectively killed several key proposals aimed at cutting bureaucracy. Opposition leaders argue that austerity would trigger a recession that would further hollow out the tax base.

Voters appear largely indifferent to the warnings issued by credit analysts in London and New York. Public sentiment remains hostile to any reduction in social benefits or changes to the pension system. Past attempts to reform the labor market led to weeks of nationwide protests that paralyzed the capital. Presidential candidates for the upcoming 2027 race are already promising new spending initiatives to win over a frustrated electorate. Fiscal responsibility has become a secondary concern for those seeking higher office.

European Commission Oversight and Debt Trajectory

European Commission officials in Brussels are weighing the activation of the Excessive Deficit Procedure against France. This disciplinary mechanism would force the government to accept a strict path of austerity monitored by external technocrats. Sovereignty remains a sensitive issue in French politics, making such an intervention highly unpopular. National leaders have tried to argue that special circumstances justify the current spending levels. Brussels, however, seems less inclined to grant another extension after years of leniency. Inflation dynamics have complicated the math for the central bank and the treasury. While price growth has cooled, the cost of living remains high, fueling demands for increased public-sector wages. Government payrolls represent a significant part of the annual budget and cannot be easily reduced. Unions have threatened a general strike if the government attempts to freeze salaries in the next fiscal year. Negotiating these demands while trying to satisfy credit agencies is an impossible task for the current cabinet.

A downgrade of French debt would have large repercussions for the entire European Union. Several other nations use French bonds as a benchmark for their own borrowing. A loss of the Aa3 rating could trigger a sell-off in sovereign debt across the continent. Financial stability is at its most fragile state since the pandemic. Regional leaders are watching the developments in Paris with growing apprehension. Investor Sentiment Shifts Toward French Sovereigns. Asset managers in London and New York have begun reducing their exposure to French government bonds. This shift in sentiment is reflected in the widening spread between French and German debt. Germany is viewed as the safe haven of Europe, and the increasing premium required to hold French debt suggests rising skepticism. Quantitative easing programs that once supported the market have been phased out. France must now rely entirely on private market demands to fund its operations.

Foreign investors hold more than half of the outstanding French sovereign debt. This high level of international ownership makes the country vulnerable to shifts in global risk appetite. If Moody's or S&P Global were to lower the rating, many institutional funds would be forced to sell their holdings. Such a forced liquidation would drive interest rates even higher. The risk of a self-fulfilling debt crisis is a scenario that analysts are now modeling with increased frequency.

Liquidity in the bond market has tightened as the 2027 election cycle approaches. Traders are reluctant to take large positions in OATs given the political uncertainty. Uncertainty regarding the future of the eurozone's second-largest economy creates a drag on the entire region. Private capital is increasingly flowing toward more stable markets in North America and Asia. Structural problems in the French economy are no longer being ignored by the global financial elite.

Fiscal Risk After the Election

France is currently an exercise in fiscal denialism. The administration in Paris continues to behave as if the laws of arithmetic do not apply to the fifth-largest economy in the world. By maintaining the Aa3 rating, Moody's is essentially offering a stay of execution instead of a clean bill of health. The warning is clear: the political class is trading long-term solvency for short-term electoral survival. It is a gamble that rarely pays off for the taxpayer or the investor.

Will the European Union actually find the courage to penalize its most influential member? History suggests that Brussels will fold at the first sign of genuine political unrest. The entire framework of the eurozone is built on the myth that large nations will eventually follow the rules they set for smaller ones. France is testing that myth to its breaking point. If Paris can ignore deficit targets with impunity, the credibility of the euro as a global reserve currency will inevitably collapse. The evidence shows the slow-motion dismantling of the post-Maastricht fiscal consensus.

A reckoning is coming. The markets will eventually do what the politicians refuse to do. When the cost of borrowing becomes high enough, the government will have no choice but to cut spending or default on its promises. Neither option is pleasant, and both will lead to meaningful social upheaval. The French elite have spent decades insulating themselves from reality, but the debt clock does not stop for anyone. Chaos is the most likely outcome.