Reserve Bank of India officials reported spiraling energy costs have overwhelmed attempts to stabilize the national currency. High crude prices, fueled by the protracted conflict involving Iran, continue to drain the foreign exchange reserves of the world's most populous nation. Efforts by central bankers to defend the Indian Rupee through aggressive market intervention have reached a point of diminishing returns. By March 31, 2026, that pressure had complicated the Reserve Bank of India’s currency defense. Data released from Mumbai indicates that the cost of importing fuel now exceeds the fiscal capacity of the state to offset currency depreciation.

Mumbai is the primary hub for these financial maneuvers, where traders have watched the rupee slide past key psychological levels. Persistent demand for dollars from oil marketing companies has created a structural imbalance that defies traditional monetary fixes. Brent crude futures stayed above the triple-digit mark for the fourth consecutive month, putting the Reserve Bank of India in a defensive crouch. Market participants noted that the central bank sold billions of dollars in the spot market to prevent a freefall, yet the currency still touched record lows against the greenback.

Oil prices dictate the health of the Indian economy more than any other single commodity.

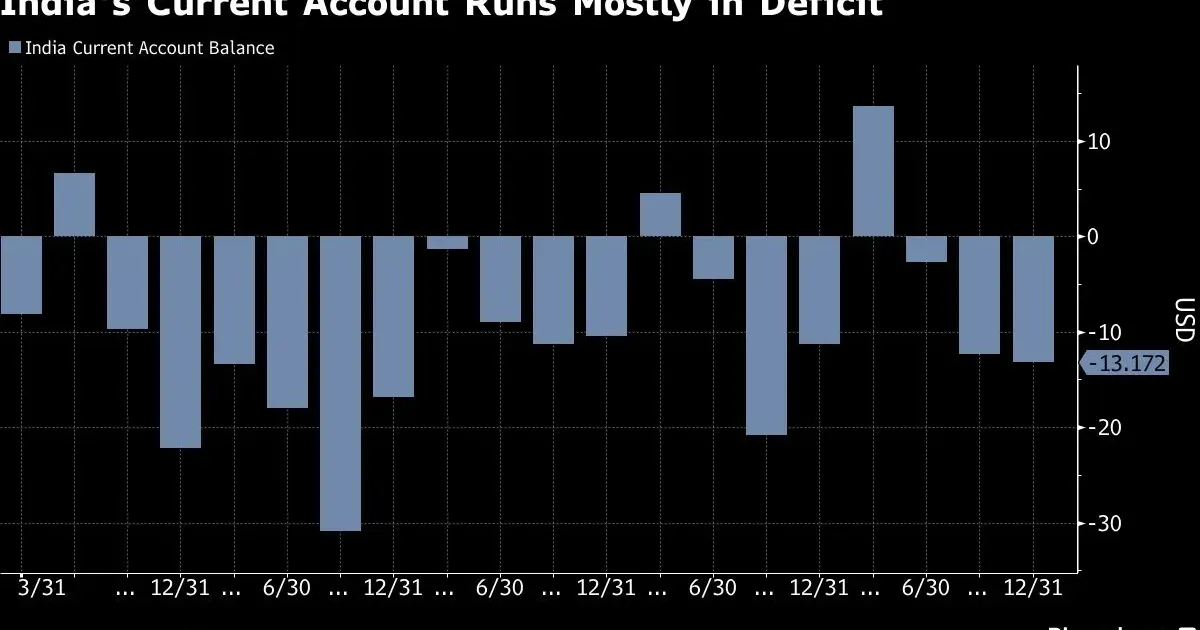

Imported energy accounts for nearly 85 percent of the country's total consumption, making the national balance sheet vulnerable to regional instability in the Middle East. Shipments from the Persian Gulf have faced insurance premium hikes and logistical bottlenecks, adding a premium to every barrel that arrives at refineries in Jamnagar or Vadinar. Economic researchers at Bloomberg indicate that for every ten-dollar increase in the price of oil, the current account deficit widens by approximately 0.5 percent of the gross domestic product. These figures translate to a direct depletion of national wealth that the central bank cannot easily replace.

India Oil Import Costs and Current Account Stress

Ministry of Finance records in New Delhi show that the annual oil bill is on track to surpass $100 billion if current price paths persist. This fiscal burden strains the current account deficit, which represents the gap between the value of goods and services imported and those exported. A widening deficit typically leads to a weaker currency, as more rupees are sold to purchase the foreign exchange required for energy transactions. Analysts observed that the current deficit has expanded to levels not seen in over a decade, testing the resilience of the financial system. Foreign institutional investors have responded to these widening gaps by pulling capital out of local equities and debt markets. This exodus of capital creates a secondary wave of pressure on the rupee, forcing the central bank to choose between protecting the currency or preserving its remaining dollar chest. Treasury officials in New Delhi have suggested that while the reserves are large, they are not infinite. The current burn rate of foreign exchange reserves suggests a strategy that prioritizes short-term stability over long-term sustainability.

Local manufacturers face surging input costs that they struggle to pass on to consumers. The closure of the Strait of Hormuz remains the primary catalyst for the current surge in global crude prices.

Policy makers in the Ministry of Finance must now struggle with the inflationary consequences of a weaker rupee. A depreciated currency makes all imports more expensive, which effectively imports inflation from global markets into the Indian household. Consumer price index readings have already begun to creep above the target range set by the Monetary Policy Committee. Rising costs for transportation and logistics are filtering through the supply chain, impacting the price of basic foodstuffs and manufactured goods across the subcontinent.

Reserve Bank of India Intervention Strategy and Results

Monetary authorities have employed a variety of tools to stem the decline, including interventions in the non-deliverable forwards market. By selling dollars in offshore markets, the central bank attempts to influence the exchange rate without immediately depleting its domestic cash reserves. These actions, however, have provided only temporary relief against the overwhelming tide of oil-related outflows. Currency traders in Singapore and London have continued to short the rupee, betting that the underlying economic fundamentals will eventually force a more clear devaluation.

"Persistent pressure on the energy front creates a structural imbalance that currency intervention alone cannot resolve indefinitely," a spokesperson for the Reserve Bank of India stated during a briefing on the current account data.

Government bond yields have risen as investors demand higher returns to compensate for currency risk. This increase in borrowing costs affects the ability of the state to fund infrastructure projects and social welfare programs. Higher yields also put pressure on corporate balance sheets, as companies with dollar-denominated debt find it increasingly expensive to service their obligations. Financial stability reports suggest that a sustained period of rupee weakness could lead to a spike in non-performing assets within the banking sector.

Rupee Exchange Rate Pressures From Global Energy Markets

Crude oil arrivals at Indian ports remained steady in volume but enormous in value throughout the first-quarter of the year. Refiners have attempted to source cheaper alternatives, yet the global supply crunch limits their options. The disruption of traditional supply lines has forced the state to pay a volatility premium that erodes the margins of the entire energy sector. Economists have noted that the inability to hedge against these price spikes has left the national budget exposed to the whims of geopolitical actors thousands of miles away.

Inflation remains a primary concern for the administration as the general election cycle approaches. High fuel prices at the pump are a politically sensitive issue that can influence voter sentiment and provoke civil unrest. Subsidies provided by the government to cushion the blow for consumers only add to the fiscal deficit, creating a cycle of debt and devaluation. Decision-makers are stuck between the need to maintain social stability and the requirement to practice fiscal discipline in the eyes of international ratings agencies. Future projections for the rupee depend heavily on the duration of the conflict in the Persian Gulf.

International energy agencies have warned that a resolution to the regional war is not imminent, suggesting that the pressure on the Indian Rupee will continue for the foreseeable future. Central bank reserves, which once stood as a powerful defense, are being tested by a commodity cycle that ignores traditional monetary boundaries. The Reserve Bank of India has exhausted many of its conventional options, leaving the currency at the mercy of global oil benchmarks. Trade balances will likely stay in the red until energy independence becomes a reality or the price of Brent crude retreats to historical norms.

Rupee Defense Pressure

Is the Reserve Bank of India fighting a ghost? For years, the narrative from Mumbai and New Delhi focused on an enormous foreign exchange war chest that could weather any storm. Yet, the current energy crisis has exposed this fortress as a facade made of paper. The central bank is not merely fighting a currency slide; it is attempting to negate the laws of physics and economics. If a country imports what it cannot produce and pays for it in a currency it cannot protect, the end result is inevitable. Intervention is not a solution. It is an expensive way to buy time that India is rapidly running out of.

The central bank should stop wasting the national wealth on futile market operations. Every billion dollars spent defending a specific exchange rate is a billion dollars that cannot be used to overhaul the nation's energy infrastructure. It is a classic sunk-cost fallacy played out on a global stage. The rupee must find its own level, however painful that may be. A weaker currency would eventually act as a natural brake on imports and a boost for exports, but the political fear of inflation prevents this necessary correction.

India remains a hostage to the Persian Gulf. The dependence is the true limit of the central bank's power. No amount of interest rate hikes or dollar sales can change that the nation's heart beats at the rhythm of an oil pump. Until the underlying structural addiction to imported hydrocarbons is broken, the rupee will always be a casualty of someone else's war. The current defense strategy is a failure.