The cash fight turns payment choice into a constitutional question. Swiss voters are weighing privacy against digital convenience. Swiss residents encountered on March 30, 2026, a rapidly shrinking network of automated teller machines and a growing list of retailers refusing paper currency. Banking institutions across Switzerland have aggressively decommissioned physical infrastructure in favor of mobile applications and contactless cards. This shift has triggered a wave of public resistance in a nation where physical money is historically linked to personal privacy and economic stability. Local shopkeepers in Zurich and Geneva now frequently post signs indicating they no longer accept high denomination notes.

Cash remains the ultimate hedge against digital failure.

Consumer surveys indicate that Swiss citizens maintain a unique attachment to the 1,000-franc note, which is one of the highest-value banknotes in circulation globally. While neighboring European nations have moved toward lower cash limits to combat money laundering, Swiss authorities have historically defended the right to use large bills for meaningful transactions. Financial institutions, however, argue that the cost of maintaining, securing, and transporting physical currency has become prohibitively expensive. This trend has resulted in the removal of over 15 percent of rural cash points over the last twenty-four months.

Retailers Shift Toward Digital Payments and Cards

Merchant groups in the service sector claim that handling cash presents a serious security risk to their employees. Robberies targeting cash-heavy businesses have pushed many restaurants and kiosks to adopt card-only policies. Handling physical money requires staff to manually count registers and make daily trips to the bank, which adds labor costs that many small businesses can no longer afford. Digital payment processors offer incentives to merchants who migrate away from currency, including lower transaction fees for the first year of exclusive digital use. Credit card companies have also integrated loyalty programs that effectively penalize those who choose to pay with francs.

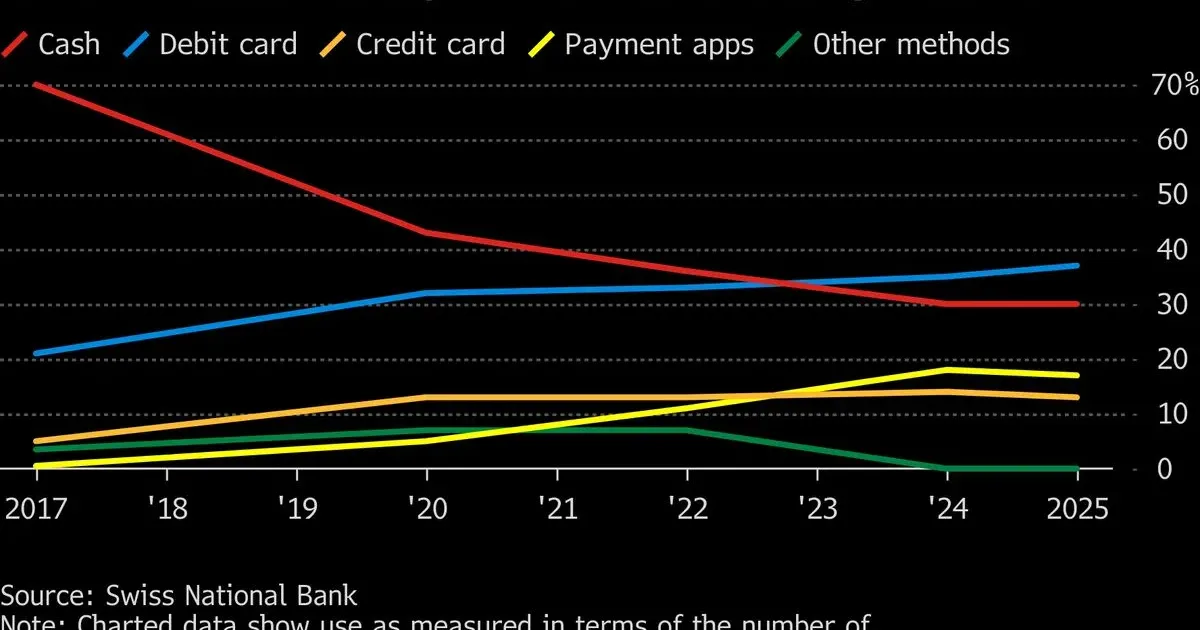

The Swiss National Bank noted in its recent report that the total value of cash in circulation peaked at $91 billion before beginning a steady decline. Younger demographics show a clear preference for instant mobile payments through apps like Twint, which has become the de facto standard for peer-to-peer transfers. High-speed internet across the Alps allows even remote mountain huts to process digital transactions with ease. This technological saturation has left traditionalists feeling marginalized in their own communities.

Rural Cantons Suffer From Automated Teller Machine Closures

Villages in the Swiss Alps find themselves in an increasingly difficult position as the nearest banking branch moves further away. PostFinance, the financial services arm of the national postal service, has closed hundreds of offices to cut costs. These closures often leave entire valleys without a single point to withdraw money or pay bills in person. Residents in these areas must travel for over an hour to reach a city with a functional ATM. Local governments have attempted to subsidize the installation of private cash machines, but the maintenance fees often exceed the municipal budget.

Cash is not just a medium of exchange in Switzerland; it is a fundamental foundation of our individual freedom and a shield against total state surveillance.

Rural business owners report that tourists often arrive with large bills that they cannot break because local banks no longer provides change services. It creates a friction point in the tourism industry, which is a major driver of the Swiss economy. Hotels in the Bernese Oberland have started warning guests in advance that they may need digital payment methods for local excursions. Pressure from these businesses has forced some cantonal governments to investigate the feasibility of state-funded cash dispensers.

Political Movements Push for Constitutional Cash Protections

Legislators in Bern are currently debating the language of a new law that would define cash as a public good. Proponents of the bill suggests that access to money is a basic right similar to access to water or electricity. Opponents argue that such a law would interfere with the freedom of contract between a buyer and a seller. They believe that if a merchant chooses not to accept cash, they should be free to do so without government interference. The debate has become a central theme in the lead up to the next round of federal elections.

Statistical data from the Swiss Retail Federation shows that 40 percent of transactions are still conducted in cash, despite the hurdles. The figure is considerably higher than in the United Kingdom or the Nordic countries. International banks view Switzerland as an outlier in its persistence to use physical currency. Pressure from global financial regulators to limit the use of high-value notes for security reasons continues to clash with the domestic desire for privacy. Swiss voters will likely have the final word on the matter at the ballot box.

Cash Protection Debate

The Swiss debate is about control as much as payment. Cash gives citizens a fallback when digital systems fail and a degree of privacy that cards and apps cannot provide. Cash access also affects tourists, rural residents and older consumers who may not want every payment routed through a private digital platform.

The referendum question will force policymakers to define what financial access means in a digital economy. A constitutional guarantee would make physical currency a public infrastructure issue.