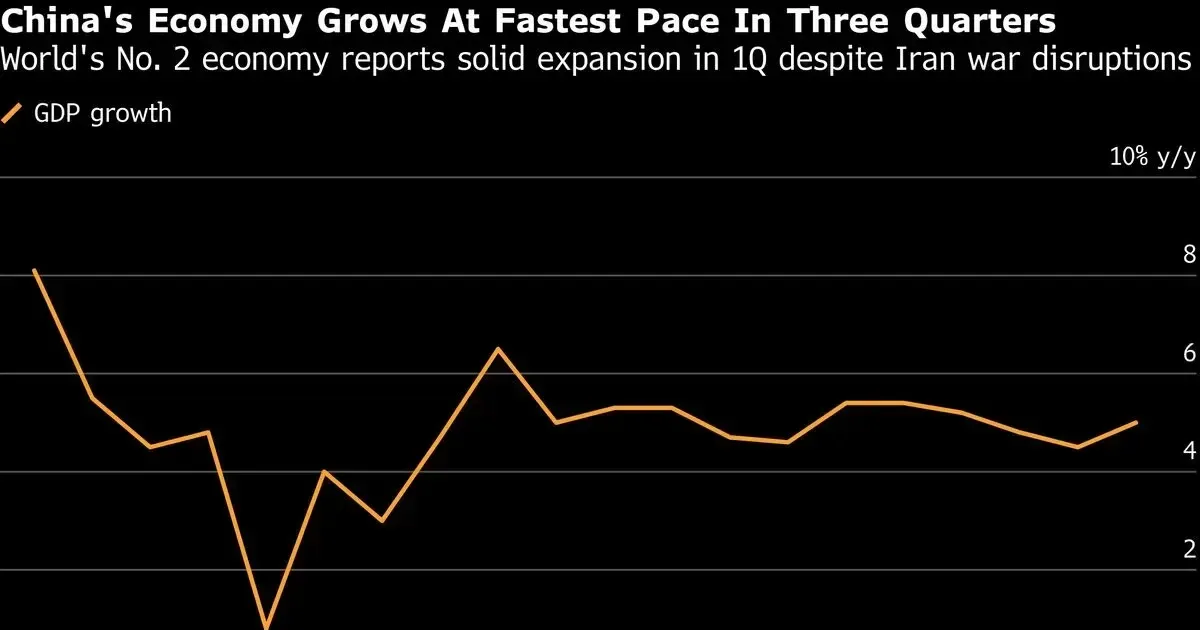

China's first-quarter data gave Beijing a stronger headline than economists expected. The first-quarter data arrived as investors searched for signs of resilience. On April 16, 2026, officials reported that China expanded its economy by 5% during the first quarter. Growth exceeded internal projections and international forecasts alike. Official data released by the National Bureau of Statistics showed that industrial production and a surge in exports provided the necessary momentum to offset lingering stagnation in the domestic property sector. This unexpected resilience occurred while global markets braced for volatility stemming from the intensified conflict in the Middle East.

Industrial production was the primary engine for this quarterly expansion. Factories across the coastal provinces reported higher use rates for high-end manufacturing and green energy equipment. Manufacturing firms focused on electric vehicles and semiconductor hardware saw double-digit increases in output. Bloomberg Economics noted that these sectors provided a meaningful buffer against the cooling demands for traditional consumer goods. Output in the manufacturing sector specifically grew by 6.1% over the same period last year.

Industrial Output Drives National Expansion

Markets reacted with cautious optimism to the industrial figures. The 5% expansion suggests that the transition toward a manufacturing-led growth model is gaining traction among state planners. Financial analysts in London and New York had previously predicted a more modest 4.6% increase. FT Global Economy reported that the state-led investment in industrial upgrades is finally showing a measurable impact on the aggregate GDP figures. Fixed-asset investment in high-tech industries rose by nearly 10% during the first three months of the year.

Export volumes provided a secondary foundation of support. Trade partners in Southeast Asia and the Global South increased their intake of Chinese machinery and electronics. Regional tensions in the Persian Gulf have redirected some shipping flows, yet Chinese exporters maintained a steady rhythm of deliveries through alternative rail and sea routes. Supply chains remained functional despite the increasing cost of marine insurance. Export growth reached 4.9% in dollar terms, a figure that surprised many who expected a sharper contraction due to geopolitical frictions.

"China’s economic growth rebounded more than expected in the first quarter of 2026, suggesting limited spillovers so far from the war in Iran," Bloomberg Economics reported.

The resilience of the export sector suggests that global demands for low-cost, high-quality industrial components persist. Fiscal tools deployed by the central government late last year began to filter through the economy in early 2026. Infrastructure spending on provincial transport networks and digital connectivity projects provided immediate jobs for the construction sector. Local governments issued a record number of special-purpose bonds to fund these initiatives. Economic planners in Beijing appear to have successfully front-loaded this spending to ensure a strong start to the fiscal year.

Export Strength Counters Weak Domestic Demand

Regional tensions surrounding the war in Iran have yet to derail the broader economic trajectory. Energy costs stayed relatively stable for industrial users because of long-term supply contracts with Siberian and Central Asian producers. Crude oil imports actually rose by 3.2% as the state continued to strengthen its strategic reserves. Analysts suggest that this energy security strategy allowed factories to maintain production schedules without the threat of power rationing. Electricity consumption by the industrial sector grew at a faster pace than the overall economy.

Investor confidence showed signs of stabilization after the release of the GDP data. Patience has become the operative word for the People’s Bank of China. Monetary policy stayed neutral throughout the quarter, as the stronger-than-expected growth figures reduced the immediate pressure for interest rate cuts. Bloomberg Economics analyzed the data and concluded that the central bank now has a wider window to monitor inflation before making its next move. Consumer prices stayed nearly flat, reflecting the ongoing struggle to spark domestic spending.

Fiscal Policy Provides Buffer Against Global War

Domestic consumption continues to be the most serious challenge for the national economy. Retail sales grew by a modest 3.4%, missing the targets set by the Ministry of Commerce. Retailers in major cities like Shanghai and Shenzhen reported that consumers are prioritizing savings over discretionary spending. Real estate investment fell by another 9.2%, indicating that the property crisis still weighs heavily on household wealth. Housing markets in lower-tier cities showed no signs of a price floor.

This lingering weakness in the property sector keeps the overall growth story lopsided. Consumer sentiment is tied to the value of apartments, which constitute the bulk of middle-class assets. Savings rates in commercial banks hit a five-year high in March. The contrast between booming factory floors and quiet shopping malls highlights the structural imbalance that the government is trying to correct. Beijing must find a way to transfer the gains from the industrial sector into the pockets of everyday citizens. Household disposable income grew by 4.1% in real terms.

Export-Led Resilience

Financial stability in a period of geopolitical volatility is rarely the result of organic strength. China’s 5% growth figure is a manufactured triumph of the state’s industrial policy, but it exposes a terrifying reliance on foreign markets that are increasingly hostile to Beijing’s dominance. The strategy of flooding the world with subsidized high-tech goods while domestic consumers hunker down is a gamble with a high probability of failure. If the United States or the European Union enacts the threatened 100% tariffs on Chinese electric vehicles, the current growth engine will stall instantly.

Can a nation truly be called a superpower when its own citizens are too afraid to spend their earnings? The gap between the 6.1% industrial growth and the anemic 3.4% retail sales is not just a statistic; it is a sign of a broken social contract. Beijing is essentially asking its population to sacrifice personal consumption to fund a global manufacturing war. This model is unsustainable in the long term. Wealth is being sequestered in state-backed industries rather than circulating through the broader population.

The Iranian conflict provides a convenient excuse for any future volatility, yet the real danger is internal. If the property market does not find a bottom by the end of 2026, the psychological weight of falling asset values will eventually crush the industrial momentum. The Chinese miracle is entering a phase of diminishing returns where every point of GDP growth requires more state intervention and more debt. Expect a sharp correction before 2027.