Bank of Japan officials stated that volatility stemming from the military conflict in Iran makes communicating interest rate shifts difficult. Policymakers currently face a dilemma as they weigh the need for monetary normalization against the unpredictable fallout of a regional war. The April 3, 2026, remarks came as traders questioned whether the bank could still guide expectations clearly. Market participants had expected a transparent signaling process similar to the strategies employed before previous hikes. Instead, the central bank has provided contradictory hints that have left the yen and bond yields in a state of suspended animation. Recent internal projections suggest that while domestic economic conditions might warrant a move, the external shock from the Middle East complicates the timing of any definitive announcement.

Traders currently perceive a high probability of a rate increase during the April meeting. Such expectations exist despite official warnings that geopolitical risks remain a primary concern for the board. Kazuo Ueda, the Governor of the central bank, has maintained a cautious tone in recent public appearances. He noted that the impact of rising energy costs on Japanese households could not be ignored in the current policy calculation. Crude oil prices jumped 12% in the last week, creating a stagflationary threat that the bank has not seen in decades. Energy importers in Tokyo have already begun passing these costs to consumers, which complicates the inflation target further.

Energy Imports Shape Japan's Rate Debate

Middle East Conflict Impacts Energy Imports and Inflation

Logistical delays have also begun to affect the broader supply chain for Japanese electronics and automotive parts. Freight rates for tankers departing the region have tripled in less than a month. Shipping companies have started rerouting vessels around the Cape of Good Hope to avoid the conflict zone. Such detours add weeks to delivery times and millions of dollars in fuel costs per voyage. Tokyo analysts believe these logistical hurdles will keep headline inflation above 2% for the foreseeable future. The challenge for the bank is determining if this inflation is transitory or if it will embed itself in wage negotiations for the coming year.

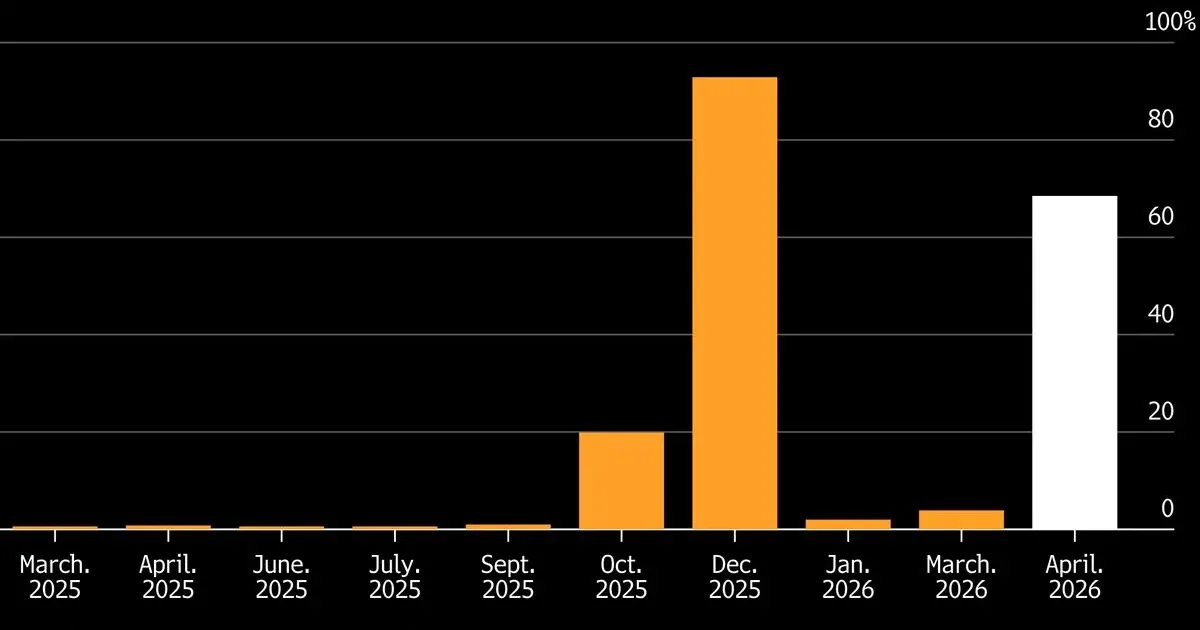

Bank of Japan Policy History and Signaling Patterns

Historical precedent shows that the Bank of Japan typically prepares the market for major shifts through a series of coordinated leaks or speeches. During the move away from negative interest rates, the bank spent months conditioning investors for the change. This coordinated messaging helped prevent a spike in 10-year Japanese Government Bond yields. Current silence from the bank's headquarters in Nihonbashi is a departure from that established strategy. Uncertainty regarding Iran has effectively muzzled the usual channels of communication. Some officials worry that a clear signal could backfire if the war intensifies and forces an immediate policy reversal.

The central bank's messaging has given traders the impression it will raise the benchmark rate this month even as authorities cite the Middle East conflict as a source of uncertainty.

Institutional investors have expressed frustration over the lack of clarity. Kazuo Ueda faces pressure from those who believe the bank is falling behind the curve on inflation. By contrast, a vocal minority of board members argues that any tightening now would be premature. They point to the fragility of domestic consumption as a reason to hold steady. Consumer spending in Japan has been sluggish for three consecutive quarters. A rate hike combined with a war-induced energy spike could potentially push the economy back into a recessionary phase.

Speculation remains widespread in the overnight index swap market. Hedge funds have increased their short positions on Japanese debt, betting that the bank will be forced to act despite the war. These investors argue that the bank cannot afford to let the yen depreciate further. A weaker currency makes imported oil even more expensive for Japanese buyers. This creates a feedback loop where the Bank of Japan must hike rates to protect the currency even if the economy is weak. The risk of a policy error is at its highest level in several years. Internal memos from the bank suggest that officials are monitoring the situation in Iran on an hourly basis.

Global Supply-chain Risks in the Persian Gulf

Global trade routes are under immense pressure as the conflict expands. Beyond oil, the Persian Gulf is an essential corridor for liquefied natural gas and chemical exports. Japan is a leading buyer of these commodities to power its industrial heartland. Any long-term closure of regional ports would require an enormous restructuring of the national energy strategy. Prime Minister Fumio Kishida has already held emergency meetings with the Bank of Japan leadership to discuss economic stability. The government is reportedly considering fresh subsidies to offset the impact of the war on energy prices. Such fiscal measures would complicate the central bank's efforts to cool the economy through higher rates.

Capital flows have become increasingly erratic since the outbreak of violence in Iran. Foreign investors are pulling money out of Japanese equities at the fastest pace since the 2008 financial crisis. They fear that a combination of high energy costs and rising interest rates will crush corporate earnings. Export-oriented companies are particularly vulnerable to these dual pressures. While a weak yen usually helps exporters, the rising cost of raw materials now outweighs the benefit of a favorable exchange rate. Industrial production figures for February showed a surprising decline in output. This data point gives the Bank of Japan another reason to remain cautious despite the inflationary pressure from the war zone.

War Risk Narrows BOJ Options

Should the Bank of Japan continue its current path of silence, it risks a catastrophic loss of credibility. The era of the central bank as an omnipotent market stabilizer ended when the first missiles flew over the Persian Gulf. Governor Kazuo Ueda is currently paralyzed by a classic trap where every available option leads to a meaningful economic downturn. If he hikes rates to save the yen, he kills the fragile recovery; if he stays pat to support growth, the currency collapses under the weight of surging oil prices.

The indecision is not a sophisticated strategy of strategic ambiguity but rather a visible display of a policy framework that has run out of runway. The bank is essentially hoping that the Iran conflict resolves itself before the April meeting, a gamble that no professional institution should ever take.

Waiting for geopolitical clarity is a fool's errand in a world where conflict is now a permanent structural feature of the global economy. The Bank of Japan has historically been too slow to adapt to external shocks, and this current hesitation mirrors the same mistakes made during the 1970s oil crises. By failing to send a clear signal, the bank allows speculators to dictate market conditions, which inherently increases the volatility they claim to despise.

The reality is that the Japanese economy can no longer survive on the life support of near-zero rates while the rest of the world faces high-inflation warfare. A decisive 25-basis-point hike in April, regardless of the noise from Iran, is the only way to signal that the central bank is still in control of the national destiny. Anything less leaves the yen exposed to another round of speculation.