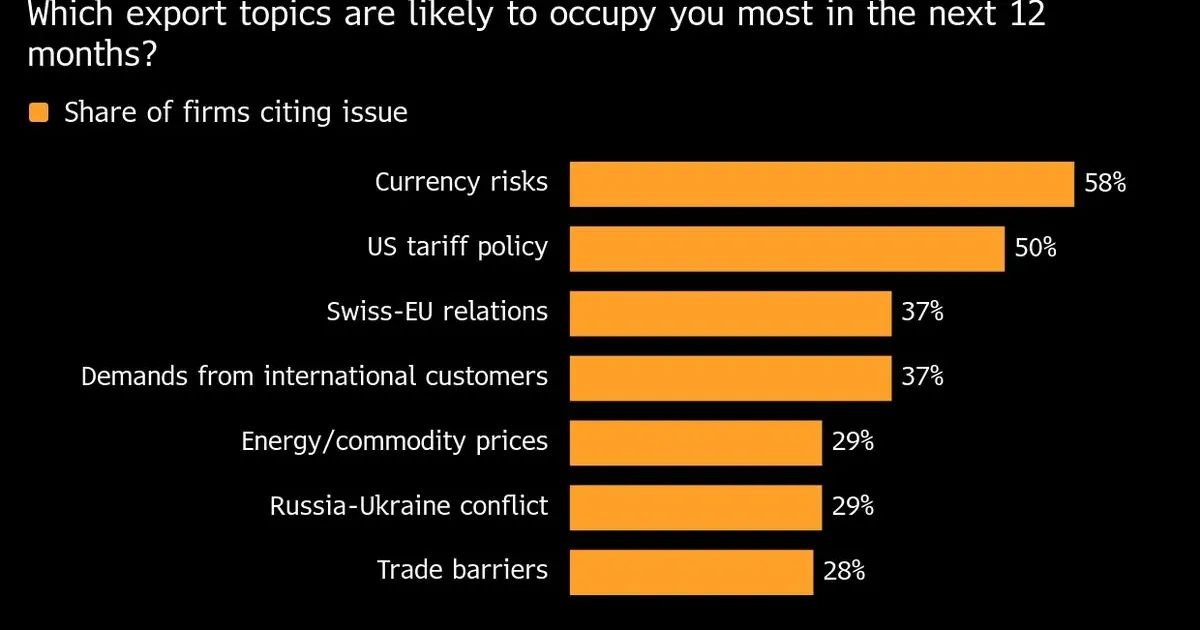

Christian Taennler watches the flickering currency monitors in his Bernese Oberland office with the practiced calm of a man who has survived a decade of economic turbulence. His manufacturing business, which specializes in precision engineering components, operates on the razor edge of global competitiveness. The relentless appreciation of the Swiss franc has transformed his daily operations from a quest for innovation into a desperate battle for price survival. While the currency remains a global symbol of stability, for local entrepreneurs, it has become an expensive burden that refuses to lighten.

Swiss exporters have historically relied on a reputation for quality to justify premium pricing, yet even the most prestigious brands are hitting a ceiling. Costs in Switzerland are already among the highest in the world, and when the franc strengthens, those costs become even more difficult to pass on to international clients. Many firms in the machine, electrical, and metal industries report that their order books are full, but their profit margins are effectively evaporating. In fact, some smaller enterprises are now operating at a loss simply to maintain their market share in the Eurozone.

Profit margins are vanishing.

Economic data from early 2026 suggests that the Swiss National Bank faces a complex dilemma as it attempts to balance price stability with the needs of the industrial core. Inflation in Switzerland has consistently remained lower than in neighboring countries, which naturally drives investors toward the franc as a safe haven. This influx of capital creates an upward pressure on the currency that traditional monetary tools have struggled to contain. To that end, the central bank has frequently intervened in foreign exchange markets, though the long-term effectiveness of these actions is more and more questioned by market analysts.

Manufacturing Sector Adapts to Currency Pressure

Adaptation has become a mandatory exercise for Christian Taennler and his peers across the manufacturing field. He has spent the last eighteen months renegotiating supplier contracts and seeking efficiencies that were previously considered impossible. Some firms have resorted to "natural hedging," which involves moving parts of their supply chain outside of Switzerland to pay for materials in euros or dollars. Still, the core labor costs remain anchored in francs, creating a persistent imbalance that cannot be solved through procurement alone.

Labor costs in the Eurozone remain sharply lower, even when accounting for the higher productivity of Swiss workers. This disparity has led several mid-sized companies to relocate entire production lines to Eastern Europe or Southeast Asia. For a country that prides itself on its industrial heritage, this migration of technical expertise is significant shift in the national economic identity. Industrial leaders argue that once a production line leaves the country, the associated research and development often follow, weakening the innovation system over time.

Relocation is no longer a choice but a requirement for many.

Investment in automation has accelerated as a direct response to the currency crisis. Firms that can afford the capital expenditure are replacing manual labor with advanced robotics to offset the high cost of the franc. But for smaller workshops with limited access to credit, the path forward is less certain. These family-owned businesses often lack the scale to automate or relocate, leaving them vulnerable to every fractional increase in the exchange rate. According to recent industry surveys, nearly twenty percent of small-scale exporters are considering a total cessation of operations if the franc continues its current path.

Swiss National Bank Policy and Inflation Targets

Monetary policy remains the primary lever for addressing currency strength, yet the SNB has limited room to maneuver. Interest rates have been adjusted multiple times to discourage speculative inflows, but the global appetite for Swiss assets remains insatiable during periods of geopolitical uncertainty. In particular, the franc's role as a hedge against volatility in the United States and the Middle East has decoupled its value from the actual performance of the Swiss economy. This decoupling means that even when domestic growth slows, the currency can continue to climb.

Small businesses are being sacrificed on the altar of currency stability, and the cost of this policy will be measured in lost jobs and shuttered factories across our industrial heartland.

Central bank officials maintain that their primary mandate is price stability, and they view a strong franc as a useful tool for keeping import prices low. The perspective offers little comfort to exporters who see their international competitiveness eroded by factors entirely outside their control. In fact, the gap between the central bank’s priorities and the needs of the industrial sector has sparked a rare public debate about the role of the SNB in supporting economic growth. Even so, the bank has resisted calls for a formal currency peg similar to the one abandoned in 2015.

Speculators continue to bet on further franc appreciation despite the risks of intervention. These market participants recognize that the Swiss economy is resilient, which ironically makes the currency more attractive to those seeking safety. By contrast, the Euro has faced its own set of challenges, making the franc-euro exchange rate a focal point of anxiety for Swiss businesses. The current rate hovering near €1.05 per franc is a level that many analysts previously considered a psychological breaking point for the export sector.

Economic Outlook for Precision Engineering Firms

Future growth in the precision engineering sector depends on the ability of firms to pivot toward high-value, niche markets where price sensitivity is lower. Christian Taennler has shifted his focus toward medical technology and aerospace components, sectors that demand exacting standards that few international competitors can match. The strategy allows him to maintain high prices, but it requires constant reinvestment in specialized machinery and staff training. For one, the barrier to entry in these markets is high, providing a temporary shield against currency-induced competition.

Meanwhile, the broader economic outlook suggests a period of stagnation for traditional manufacturing. Export volumes dipped 4.2 percent in the final quarter of last year, a trend that is expected to continue through the middle of 2026. While the pharmaceutical and luxury watch sectors have shown more resilience, the "bread and butter" of Swiss industry, the machinery and tool-making workshops, are bearing the brunt of the pain. These businesses form the backbone of the Swiss middle class, providing high-skilled employment in rural regions like the Bernese Oberland.

Government subsidies are rarely discussed in the Swiss context, as the nation prides itself on a hands-off approach to industrial policy. Instead, the focus has shifted toward tax incentives for research and development to help firms stay ahead of the technological curve. Yet, these measures take years to yield results, while the currency pressure is an immediate, daily reality. The Swiss export model is currently undergoing its most significant stress test in a generation. Success for these firms now depends as much on their accounting departments as it does on their engineering prowess.

The Elite Tribune Perspective

Betting against the Swiss franc has historically been a fool’s errand, but the current obsession with currency stability is hollowing out the very industrial base that gave the franc its value. The Swiss National Bank operates with an ivory-tower detachment that borders on negligence, prioritizing inflation targets while ignoring the slow-motion collapse of the nation's manufacturing soul. It is easy to champion a strong currency from a mahogany desk in Zurich, but the view is sharply grimmer from the factory floor in a mountain valley where margins have been squeezed to the point of extinction.

Switzerland is effectively exporting its industrial capacity to neighboring countries, trading long-term economic diversity for short-term price stability. It is not a lasting strategy for a nation with no natural resources other than its human capital and its reputation for precision. If the SNB continues to treat the industrial sector as a secondary concern, they may find themselves presiding over a pristine, stable currency that has no actual economy left to back it up.

The time for polite intervention has passed; what is required now is a radical reassessment of how a small nation protects its productive core from being crushed by its own success. The franc is no longer just a safe haven; it is a cage.