War Fears Push Japan Factory Output to 12-Year High now turns on the gap between the announcement and the institutional response. The immediate question is who absorbs the pressure once the headline moves into practical consequences. That makes the follow-up more important than the first public reaction. Officials, markets and affected communities will read the next step through their own exposure. April 23, 2026, saw Japan register its highest manufacturing activity in over a decade as regional instability in the Middle East forced a large shift in industrial strategy. Manufacturers across the archipelago ramped up production at a speed not seen since 2014, responding to fears that shipping lanes could face indefinite closures. This surge in factory output stems from a practice known as frontloading, where companies accelerate production schedules to build inventories before anticipated supply-chain collapses occur. Economic indicators suggest that the sudden expansion is less about rising global demand and more about an urgent defense against logistical paralysis. today

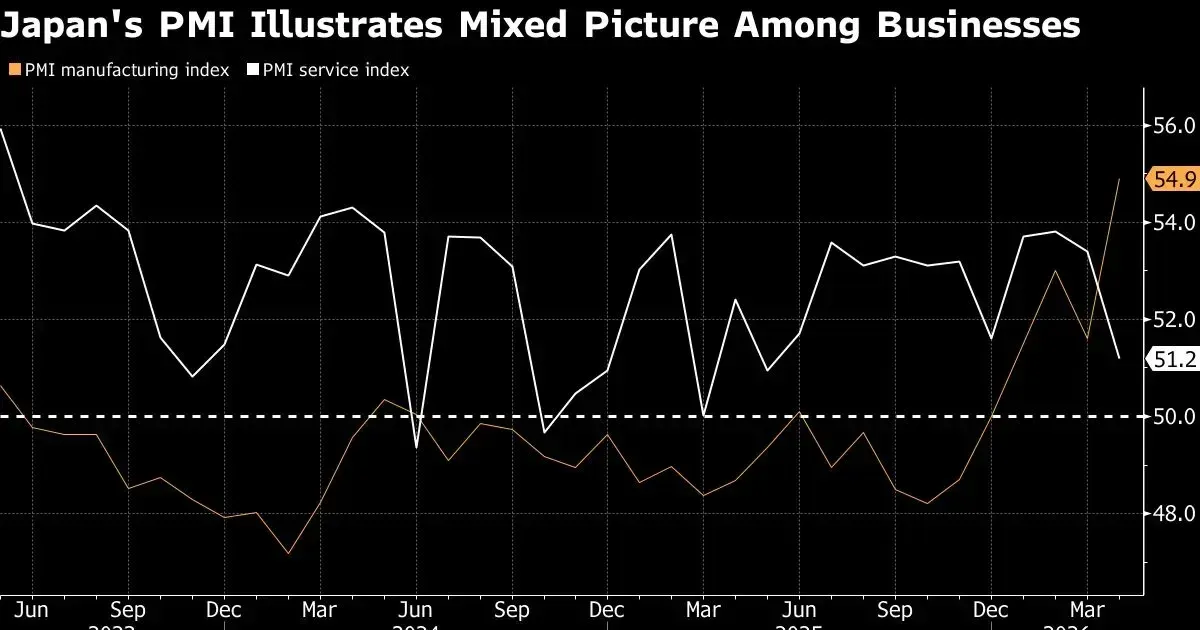

Reports from Bloomberg Economics confirm that the Purchasing Managers’ Index (PMI) surged past expectations, signaling a strong but perhaps temporary expansion. Business leaders in Tokyo and Osaka are ordering raw materials in bulk to preempt price hikes driven by volatile energy markets. Industrial production levels increased across several key sectors, including automotive parts, electronics, and heavy machinery. While a higher PMI usually signals economic health, the current reading reflects a survivalist instinct within the Japanese corporate sector.

Bloomberg Economics data indicates that factory output reached its highest point in 12 years during the last fiscal quarter. Analysts attribute this acceleration to the heightening conflict in the Middle East, which has already disrupted traffic through the Suez Canal. For a nation as dependent on imported energy and raw materials as Japan, any threat to maritime security creates immediate pressure to secure finished goods. Manufacturers are moving away from the traditional just-in-time delivery model in favor of a just-in-case strategy. Production lines are running at full capacity to ensure that domestic and international commitments can be met even if shipping costs continue to climb.

Japanese Manufacturing Growth and Global Supply Chains

Supply-chain reliability remains a primary concern for the Ministry of Economy, Trade and Industry. Global shipping routes, particularly those passing through the Red Sea, are currently subject to extreme delays and rising insurance premiums. Japanese firms rely on these routes for a meaningful portion of their trade with Europe and parts of Asia. Because shipping times have doubled for some components, factories must produce and ship goods well in advance of their actual delivery dates. Failure to frontload production could result in empty shelves and stalled assembly lines in secondary markets.

Inventory accumulation has reached record levels as companies hedge against geopolitical risk. Managers are prioritizing the completion of existing orders while the logistics window remains open. Domestic warehouses are reaching capacity limits as finished products wait for available cargo space on outbound vessels. Export-oriented firms are particularly sensitive to these shifts, as their revenue depends on the timely arrival of goods in Western markets. The increased output is a logical response to the reality of a fragmented global trade network.

According to Bloomberg Economics, the rapid ramp-up in Japanese manufacturing is a hedge against the widening consequences of the Middle East conflict on global logistics.

Energy prices matter in these manufacturing calculations. Japan imports nearly all of its petroleum and liquid natural gas, making its industrial base highly sensitive to Middle East stability. Rising crude oil prices increase the cost of running factories and transporting goods. By accelerating production now, companies hope to lock in current energy costs before further escalations drive prices higher. Industrial energy consumption has spiked alongside the increase in factory output, placing temporary strain on the national power grid. While Japan ramps up production, other manufacturing hubs are also feeling the pressure of shifting global supply chains due to regional instability.

Middle East Conflict and Industrial Risk Management

Regional instability has historically pushed Japanese firms to diversify their supply chains, yet the current conflict presents a unique set of challenges. Unlike localized disruptions, the current war threatens the core arteries of international commerce. Shipping conglomerates have diverted vessels around the Cape of Good Hope, adding weeks to transit times. Such delays force manufacturers to maintain larger buffers of both raw materials and finished products. The cost of this additional inventory is being absorbed by corporations in the short-term to maintain market share.

Logistics managers are reporting that shipping containers have become increasingly difficult to secure. This scarcity drives up the cost of every unit produced, creating a feedback loop of inflationary pressure. Manufacturers are responding by maximizing every available production hour before logistical constraints become overwhelming. The current data reflects a race against time. If the conflict extends into the next year, the current pace of production may become unsustainable due to rising overhead costs.

Japan continues to experience these pressures more sharply than its peers in North America. Its geographical position and lack of domestic natural resources leave it uniquely exposed to maritime disruptions. While the United States can rely on domestic energy production, Japanese factories are at the mercy of the tanker fleets. This vulnerability dictates the aggressive production schedules observed in the latest PMI reports. Every day of continued conflict in the Middle East adds to the urgency felt on the factory floors of Nagoya and Saitama.

Monetary Policy and Bank of Japan Reactions

Central bank officials are monitoring the output surge for signs of sustainable growth. The Bank of Japan has maintained a cautious stance on interest rates, wary of stifling an economy that is finally seeing movement in the manufacturing sector. However, the nature of this growth presents a dilemma for policymakers. If the production spike is driven solely by war-related frontloading, it may be followed by a sharp contraction once inventories are filled. Shifting policy based on a temporary surge could destabilize the broader financial system.

Inflation targets are also affected by the sudden increase in industrial activity. High demand for labor and raw materials puts upward pressure on prices, potentially pushing inflation above the central bank’s comfort zone. Wages in the manufacturing sector have seen modest increases as factories compete for workers to staff extra shifts. These labor costs, combined with higher energy prices, contribute to a complex inflationary environment. The Bank of Japan must distinguish between healthy demand-driven inflation and the cost-push inflation resulting from geopolitical crises.

Currency fluctuations further complicate the industrial landscape. A weaker yen makes Japanese exports more competitive but increases the cost of the imported energy required to produce them. Manufacturers find themselves in a delicate balancing act. They must maximize the benefits of a favorable exchange rate while reducing the impact of expensive inputs. The current PMI data suggests that, for now, the drive to secure market share through increased output is the dominant strategy.

Expectations for the next quarter remain tied to the duration of hostilities in the Middle East. If a ceasefire is reached, the need for frontloading will diminish, likely leading to a cooling of factory activity. By contrast, an escalation will only intensify the pressure on Japanese manufacturers to produce as much as possible, as quickly as possible. The 12-year high in production levels matches data from the 2014 industrial expansion.

Factory Resilience

History rarely rewards those who mistake panic for progress. The current surge in Japanese factory output is not a sign of a renewed industrial titan, but rather a frantic attempt to build a bunker before the storm hits. When a nation’s PMI hits a 12-year high during a global security crisis, the savvy observer looks not at the growth, but at the fear driving it. It is a survivalist economy, one that has realized its just-in-time miracles are useless when the Red Sea is a combat zone.

The Japanese corporate structure is effectively gambling on its ability to outrun a total collapse of global logistics. By frontloading production, these firms are tying up huge amounts of capital in stagnant inventory. It is a defensive crouch disguised as an offensive sprint. If the Middle East conflict stabilizes tomorrow, Japan will be left with an enormous oversupply and no buyers for the surplus. The Bank of Japan is right to be skeptical because this data is an anomaly born of desperation.

Global trade is fracturing into regional blocs, and Japan is caught in the middle with no domestic energy to sustain itself. This 12-year peak is a warning. It signals that the era of efficient, low-cost global trade is ending. What we see today is the last gasp of a system trying to produce its way out of a geopolitical trap. The result will be a painful correction.