Central banks in India and Romania are being forced to treat the Iran conflict as a monetary-policy event. Oil near $110 per barrel, currency pressure and capital flight have narrowed the space for rate cuts.

The pressure was clear as the Reserve Bank of India prepared for its first decision since the latest Gulf escalation. On April 7, 2026, Romania faced a separate version of the same problem: high inflation, weak confidence and limited room to ease.

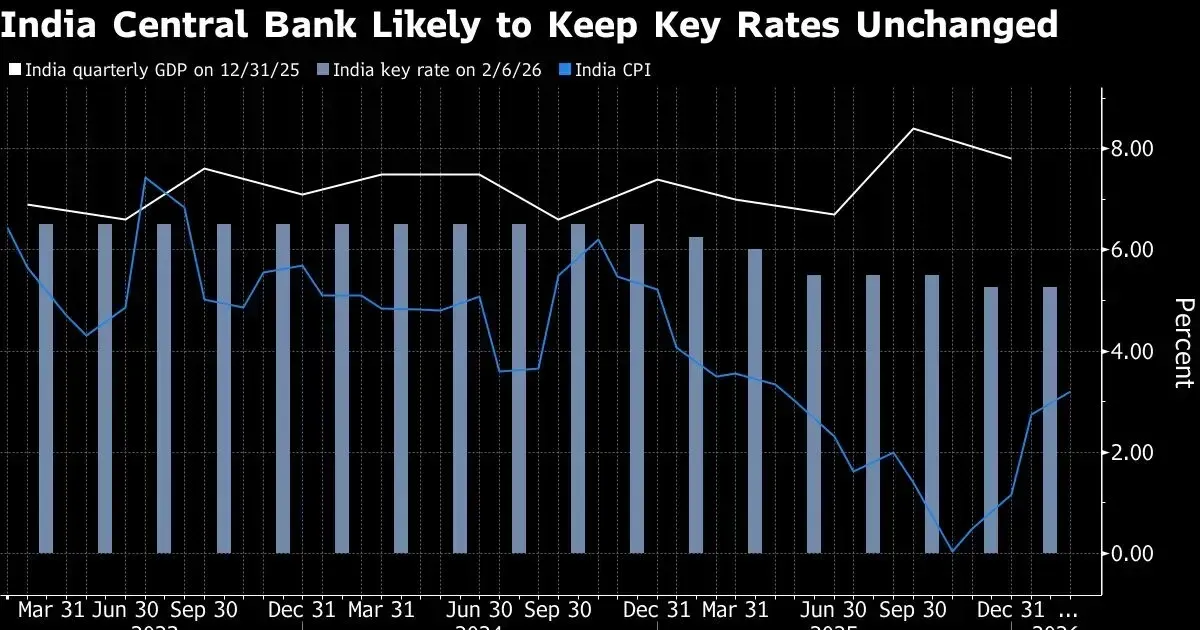

India Confronts Rupee Depreciation and War

Currency depreciation is a hidden tax on the Indian population. As the rupee falls, the cost of technology, fertilizer, and fuel increases. Lower income households spend a larger share of their earnings on these essentials. The Reserve Bank of India has intervened in the spot market to smooth volatility. Such interventions have reduced total foreign reserves by 15 billion dollars in 30 days. Traders expect the rupee to test new lows if the conflict in the Middle East expands.

Supply-chain disruptions are compounding the misery. Shipping delays have added ten days to the average transit time for goods moving between Mumbai and Rotterdam. Indian exporters face higher freight charges, reducing their competitiveness in global markets. The central bank cannot fix these logistical bottlenecks through interest rate adjustments alone. Monetary policy is a blunt instrument despite physical trade barriers. Industrial production grew by only 2.1 percent in February.

Romania Maintains European Union Highest Interest Rates

Bucharest remains an outlier in the European monetary landscape. Most neighboring countries have begun a tentative easing cycle to stimulate stagnant economies. Romania cannot afford such luxury while its fiscal deficit stays above 6 percent of gross domestic product. The National Bank of Romania must compensate for government overspending by keeping credit tight. Loose fiscal policy often requires tight monetary policy to prevent an inflationary spiral. Political pressure to cut rates ahead of elections has so far been ignored by central bank governors.

Inflation in Romania is more stubborn than in the rest of the Eurozone. Food prices have risen by 14 percent year-on-year. Shortages of sunflower oil and grain have worsened the situation. The National Bank of Romania projects that inflation will stay above the target range until 2027. The long-term forecast suggests that interest rates will stay elevated for the foreseeable future. Borrowing costs for small businesses currently exceed 10 percent in many sectors.

Oil Price Surges Reshape Monetary Forecasts

Energy security has become the defining theme of 2026. Countries without serious domestic production are at the mercy of global spot prices. The Reserve Bank of India monitors the price of the Indian crude basket daily. If prices exceed 120 dollars, the central bank may be forced to hike rates rather than just holding them. Such a move would be a desperate attempt to stop capital outflow. No one wants to hold assets in a currency that is losing its purchasing power so quickly.

Global demand for oil has not fallen despite the high prices. Emerging economies require energy to maintain basic infrastructure. India and Romania both show high energy intensity in their industrial sectors. It means they use more energy per unit of GDP than services-based economies like the United Kingdom. So, they are more vulnerable to the current price shock. Refineries in India have started looking for alternative suppliers in Africa and Latin America.

Market participants are repricing the duration of the current inflationary wave. Initial hopes for a short-lived spike have vanished as the war enters its third month. The National Bank of Romania has warned that secondary effects are now appearing in service sector wages. Workers are demanding double-digit raises to keep up with the cost of bread and electricity. If a wage-price spiral takes hold, central banks will have to stay restrictive for years. The scenario would lead to a period of stagflation characterized by zero growth and high prices.

International cooperation on monetary policy has fractured. The Reserve Bank of India is increasingly looking toward BRICS partners for currency swap lines. These arrangements allow trade to continue without relying on the US dollar. However, these mechanisms are still in their infancy and cannot yet replace the liquidity of the global financial system. For now, the path of interest rates in New Delhi and Bucharest depends entirely on the moves of tankers in the Persian Gulf. The first cargo ship to be sunk changed every economic model in the world.

On April 7, 2026, the Reserve Bank of India prepares for its first interest rate decision since the start of hostilities in the Persian Gulf. Geopolitical instability in Iran has triggered a steep decline in the value of the rupee. Currency traders now watch for signals that Governor Shaktikanta Das will prioritize exchange rate stability over domestic growth incentives. Inflationary pressures have mounted rapidly across the subcontinent. Bloomberg Economics suggests the central bank has little room for maneuver that might further weaken the national currency.

Central Banks Are Buying Time

Holding rates steady is not a solution to an oil shock. It is a way to buy time while officials try to protect currencies and prevent inflation expectations from moving higher.

India and Romania face different domestic conditions, but the constraint is similar: easing too early could weaken the currency and import more inflation through fuel, food and transport costs. That time is valuable but limited. If energy costs stay elevated and trade routes remain unstable, central banks will be managing imported pressure with tools built mainly for domestic demand.