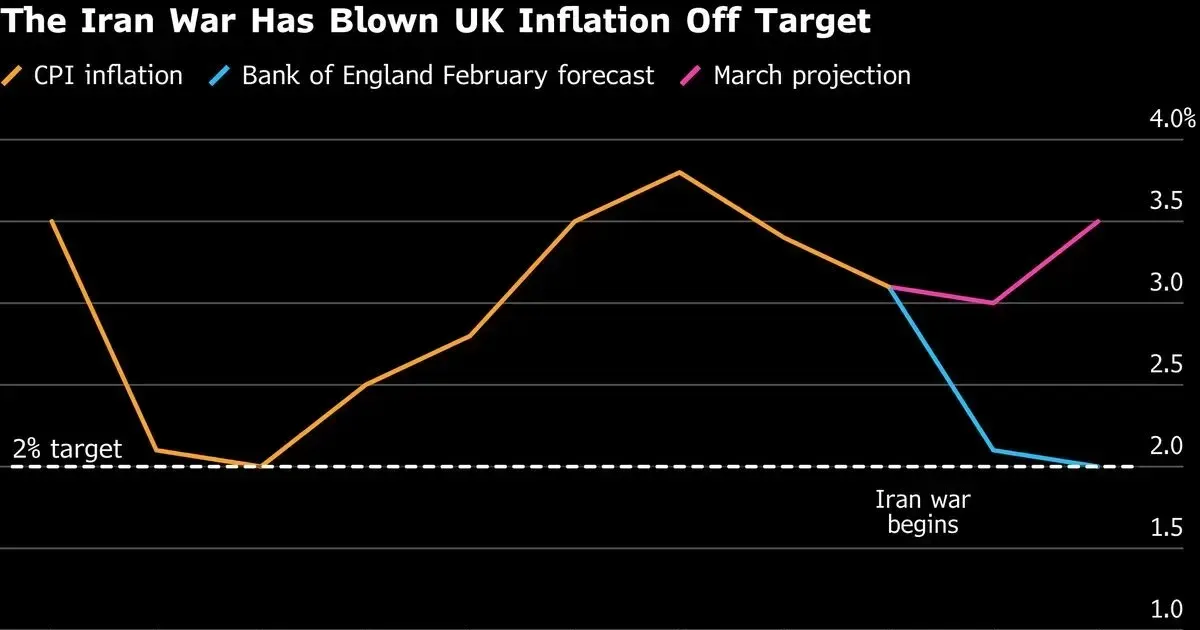

Iran War Drives UK Inflation to 3.3 Percent in March now sits inside a wider institutional test. The headline result matters, but the follow-through will decide whether the decision has durable force. Officials and markets are already reading the details through their own exposure. On April 22, 2026, the Office for National Statistics confirmed that the conflict involving Iran has forced UK inflation to climb higher than anticipated. Rising petrol costs, triggered by the intensifying regional war, pushed the annual rate of the Consumer Prices Index to 3.3 percent for the month of March. This figure is a striking jump from the 3.0 percent recorded in February, matching the consensus forecasts of City economists who had braced for a volatile energy market. Britain now faces its most meaningful fuel price surge in more than three years, adding immediate pressure to household finances across the country.

Fuel Prices Hit Three-year High

Petrol and diesel costs at the pump were the primary engine for the inflationary spike reported this week. Crude oil prices hovered near $100 a barrel throughout the period, largely due to the ongoing closure of the Strait of Hormuz. Because this narrow waterway handles approximately one-fifth of global oil consumption, its obstruction has created a persistent supply bottleneck that domestic retailers have passed on to consumers. Households in the United Kingdom are seeing the direct consequences of geopolitical instability at the filling station.

Energy costs often act as a lead indicator for broader economic pain, and the current figures suggest a widespread impact. Beyond the immediate rise in fuel, the cost of transporting goods across Britain has also trended upward, influencing the price of food and retail services. Official data shows that the March increase was the sharpest recorded since early 2023. This rapid acceleration in prices has eroded the modest gains in real wages that workers experienced during the previous winter months.

Energy security remains a critical vulnerability for the British economy as the war between US-Israeli forces and Iran persists. While a temporary ceasefire extension offered some hope to global markets, the underlying supply constraints have not vanished. Experts at Bloomberg Economics noted that the March data only captures the initial phase of the price shock. Retailers have signaled that if crude remains at these elevated levels, a second wave of price hikes for domestic energy bills will likely arrive in July.

Rachel Reeves Faces Fiscal Headroom Crisis.

Chancellor Rachel Reeves is confronting an unstable budgetary situation as the cost of the conflict filters through the national accounts. Research from the Resolution Foundation suggests that a prolonged Middle Eastern war could decimate the fiscal headroom established in the previous autumn budget. Current analysis indicates that the Treasury could lose three-quarters of its financial cushion if inflation and energy prices remain on their current trajectory. Such a scenario would severely limit the government's ability to fund public services or offer tax relief.

A severe but plausible scenario, in which the conflict intensifies and delivers the largest hits to the economy, would result in government borrowing increasing by £16bn a year in 2029-30.

Resolution Foundation analysts warned that the projected increase in borrowing would fundamentally alter the government's long-term spending plans. This escalation threatens to add £16 billion a year to the national debt by the end of the decade. Economic resilience depends on stable borrowing costs, yet the inflationary environment usually demands higher yields on government bonds. Reeves must now balance the need for increased military and energy spending against the reality of a shrinking tax base and rising debt interest payments.

Borrowing requirements are already under strain due to the slowdown in domestic productivity. If the conflict in the Middle East continues to sap consumer confidence, the Treasury may find itself forced into emergency fiscal measures. Business leaders have expressed concern that the current volatility will deter private investment, which the government had hoped would drive growth. The margin for error in the upcoming fiscal cycle has almost entirely disappeared.

Bank of England Holds Rates Steady

Bank of England policymakers are expected to maintain the current interest rate despite the headline inflation jump. While the central bank typically raises rates to cool a warming economy, the current inflation is driven by external supply shocks rather than domestic demand. Raising rates now would risk stifling the already fragile recovery of the UK economy. Sources cited by the Financial Times indicate that the Monetary Policy Committee will look through the temporary fuel spike during its meeting next week.

Maintaining interest rates at current levels offers some relief to mortgage holders, but it does little to address the rising cost of living. Central bankers are in a difficult position because they cannot control the price of global oil. If they tighten policy too aggressively, they could trigger a recession. By contrast, if they allow inflation to become embedded in wage expectations, the long-term damage could be even more severe. Most analysts expect a cautious hold as the committee waits for more data on the war's duration.

Monetary policy remains a blunt instrument despite geopolitical warfare. Markets have priced in a period of higher-for-longer rates, reflecting the reality that inflation is unlikely to return to the 2 percent target while the Strait of Hormuz is contested. Investor sentiment has turned cautious, with many shifting assets toward traditional safe havens. The pound has shown relative stability against the euro, though it has struggled to maintain its position against a strengthening US dollar.

Energy Security and the Strait of Hormuz

Geopolitical analysts emphasize that the Strait of Hormuz is the world's most important oil transit point. Any sustained closure there guarantees high prices regardless of domestic production levels in the North Sea. The United Kingdom imports a significant part of its liquefied natural gas and refined petroleum products, making it highly susceptible to maritime disruptions. Military experts suggest that until the naval routes are fully secured, the global energy market will remain in a state of high alert.

Oil prices saw a minor retreat following news of diplomatic discussions, yet they remained stubbornly high. The impact of the conflict is, as analysts frequently observe, highly uncertain and subject to sudden shifts. Domestic energy security has become the focal point of political debate in Westminster, with opposition parties calling for faster investment in renewables. However, the immediate crisis is one of liquid fuel supply, which green energy cannot solve in the short term.

Supply-chain resilience is now the primary concern for the ONS as it prepares for the April data release. Transportation costs for heavy industry have risen by 5 percent in the last six weeks alone. These costs are rarely absorbed by corporations and almost always find their way to the consumer. The snapshot provided by the March figures is a clear indication that the British economy is now paying a war premium on almost every basic commodity.

Inflation Pressure

Complacency in Whitehall regarding energy diversification has left the British public exposed to the whims of Middle Eastern volatility. For decades, successive governments prioritized low-cost global supply chains over national energy sovereignty, and the March inflation figures represent the bill finally coming due. The UK finds itself in a strategic trap where its fiscal health is dictated by a naval blockade thousands of miles away. It is not a failure of market mechanics but a failure of geopolitical foresight.

Chancellor Rachel Reeves cannot tax or spend her way out of a global supply shock that is fundamentally physical in nature. The Resolution Foundation’s warning of a £16 billion borrowing surge is likely conservative given the potential for the conflict to expand into a broader regional war. If the Strait of Hormuz stays closed for another six months, the inflationary pressure will move beyond fuel and into the very fabric of British industrial capacity. The Bank of England’s decision to hold rates is a quiet admission of powerlessness. They are spectators in a game played by generals and regional hegemons. Stability is now a relic of the pre-war era. Investors should prepare for a decade defined by stagflation and the permanent erosion of the 2 percent inflation target. The myth that the UK could transition to a high-growth economy while remaining tethered to the world's most volatile geography has been shattered. Future budgets will not be about building hospitals or schools; they will be about subsidizing the basic survival of a nation that forgot how to fuel itself.