Rising US-Iran Tensions Push Dollar to 10-Day High now turns on the distance between the first headline and the institutional response. The practical question is who absorbs the pressure once the decision moves into real systems. Global currency markets shifted on April 23, 2026, when the US dollar surged to its highest level in 10 days. Reports of intensified hostilities between the United States and Iran forced a rapid reappraisal of geopolitical risk among institutional traders. Movement in the Greenback effectively erased recent gains in risk-on currencies that had benefited from earlier hopes of a diplomatic de-escalation. Military maneuvers in the Persian Gulf triggered an immediate flight to safety during early trading sessions. Safe-haven demand accelerated, pushing the dollar higher against every major peer in the G10 group. Investors who previously anticipated a cooling of regional friction moved to liquidate positions in emerging market currencies.

Intelligence regarding new military postures near the Strait of Hormuz caused oil futures to climb. Financial institutions reacted by hedging against potential energy supply disruptions, further strengthening dollar-denominated assets. Silence from the leadership in Teheran often creates a vacuum of information that markets fill with worst-case scenarios. Uncertainty drives the premium on US Treasury bonds and the currency that backs them. Foreign exchange desks in New York reported a spike in volume during the first two hours of trade. Buy orders for the dollar outpaced sell orders by a meaningful margin as funds braced for retaliatory strikes. Liquidity in the Euro and Sterling markets thinned as the day progressed.

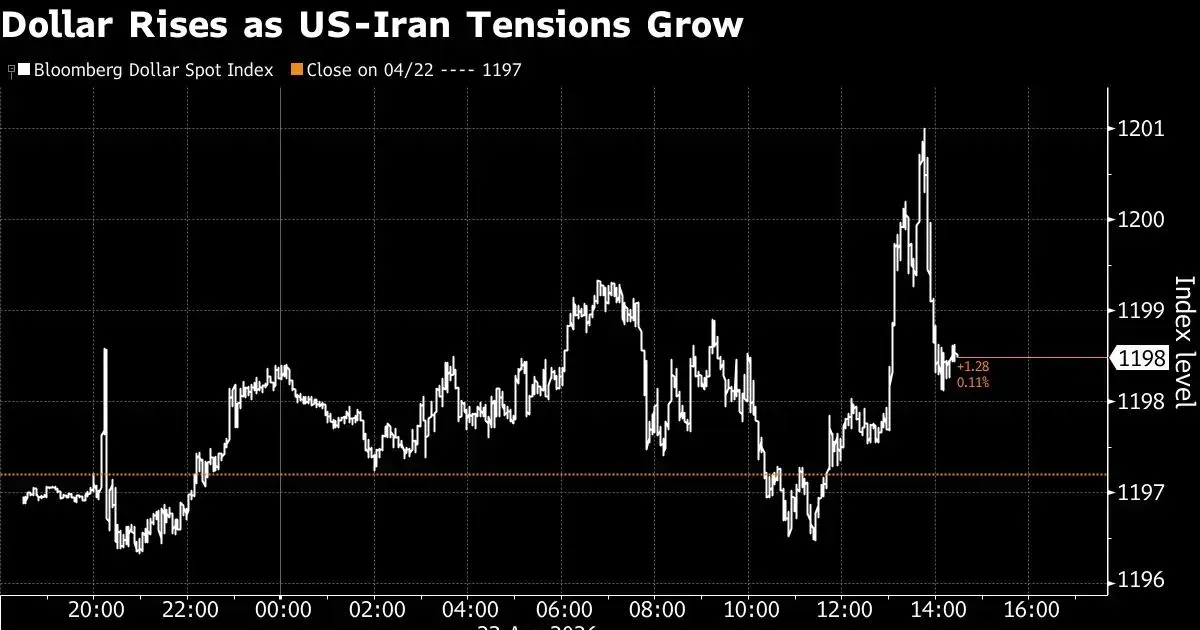

Middle East Hostilities Drive Currency Volatility

Hostilities between Washington and Teheran reached a new threshold of intensity. Markets had been pricing in a period of relative calm, but fresh reports of drone activity and naval standoffs shattered that complacency. Risk appetite vanished within minutes of the initial news bulletins. Analysts at Bloomberg Economics observed that the sudden spike reflects deep anxiety over energy security and maritime trade routes. Any disruption in the Strait of Hormuz leads to a stronger dollar. The currency stays the primary denomination for global oil transactions. Speculators who had bet on a weaker dollar found themselves forced into a short-covering rally.

Technical resistance levels for the DXY Index broke early in the day. Breaking above the 10-day moving average signaled a shift in short-term momentum. Resistance now sits at the month-to-date high, which traders expect the market to test if military rhetoric continues. Defense contractors saw their share prices move alongside the currency. Geopolitical friction is a reliable catalyst for defense spending projections. Institutional portfolios are shifting toward capital preservation rather than growth-oriented strategies. This single-day move represents the sharpest volatility spike of the current quarter.

Dollar Performance Against G10 Rivals

Major currencies felt the pressure of a resurgent Greenback. The Euro fell to its lowest point against the dollar since the start of the month. Weakness in the Eurozone is worsened by the region’s dependence on imported energy. Investors view the US economy as more insulated from Middle Eastern energy shocks due to domestic shale production. Sterling also struggled to maintain its footing despite hawkish signals from the Bank of England. Domestic inflation concerns in the UK were eclipsed by the global rush toward dollar liquidity. Safe-haven flows prioritized liquidity over yield differentials. The Japanese Yen, often a competitor for safe-haven flows, failed to match the dollar's pace. Major firms like Exxon Mobil have warned that energy supply disruptions could significantly impact bottom lines.

A report from Bloomberg Economics stated that intensifying hostilities in the Middle East dampen optimism for the potential end to the conflict.

Central banks in Asia intervened in the markets to stabilize their local currencies. Rapid depreciation of the Won and the Yuan can destabilize regional trade balances. Officials in Seoul and Beijing are closely monitoring the dollar’s trajectory. Excessive dollar strength increases the cost of servicing dollar-denominated debt for emerging markets. Global debt obligations become much more expensive when the Greenback rallies. Market participants are now pricing in a 'geopolitical premium' that could persist for weeks. Hedging costs for currency swaps have risen to their highest levels since the previous year.

Escalating Conflict Impacts Global Supply Chains

Shipping lanes in the Middle East handle approximately one-fifth of the world’s oil consumption. Threats to these lanes immediately translate into higher insurance premiums for cargo vessels. Higher shipping costs fuel global inflationary pressures. Inflationary data typically prompts the Federal Reserve to maintain higher interest rates for longer periods. High-interest rates attract foreign capital, which further strengthens the dollar. Economic cycles are becoming increasingly sensitive to kinetic military actions. Logistics firms are rerouting vessels around the Cape of Good Hope to avoid the conflict zone. Delays in delivery schedules add another layer of complexity to global manufacturing. Port congestion in the Mediterranean has begun to increase as ships seek alternative docking locations.

Semiconductor manufacturers are watching the situation with concern. Specialized gases used in chip production often originate from regions adjacent to the conflict. Supply-chain fragility remains a primary concern for technology executives in Silicon Valley. Corporate earnings calls are now dominated by questions regarding geopolitical resilience. Diversification of supply sources is a multi-year project that cannot address immediate crises. Short-term volatility in the dollar makes long-term capital expenditure planning difficult. Financial controllers are prioritizing cash hoarding to manage potential shocks. Most companies are opting for conservative guidance in their quarterly reports.

Federal Reserve Response to Geopolitical Risk

Federal Reserve officials have remained quiet regarding the latest market moves. Traditional policy dictates that the central bank looks through short-term geopolitical shocks. Sustained energy price increases could force a change in that stance. If oil prices sustain levels above $100 per barrel, the inflation outlook will require revision. Traders are scanning every public appearance by Fed governors for clues on policy shifts. Yields on the 2-year Treasury note rose alongside the dollar. Bond markets are signaling that the 'higher for longer' interest rate environment is here to stay. Capital flows into US fixed-income products provide a structural floor for the currency. Private equity firms are slowing their deployment of capital until the regional situation stabilizes.

Bank of Japan officials are in a particularly difficult position. A strong dollar forces the Yen lower, which increases the cost of energy imports for Japan. Resource-poor nations suffer most when the dollar and oil rise simultaneously. Global economic growth forecasts for the remainder of 2026 are already being adjusted downward. Lower growth typically hurts commodity-sensitive currencies like the Australian and Canadian dollars. Both currencies traded lower against the Greenback throughout the afternoon. Market sentiment is currently dominated by fear of escalation. Options markets show a serious bias toward further dollar calls.

Dollar Pressure

Is the global financial system finally admitting that the era of cheap energy and stable borders has ended? Financial markets reacted to the US-Iran friction with a predictable flight to the dollar, but this move exposes a deeper, more systemic vulnerability. We are no longer living in a world where geopolitical flare-ups are transitory blips on a screen. Instead, these events are becoming the primary drivers of capital allocation, overriding traditional economic fundamentals like employment data or retail sales.

The surge in the dollar is not a sign of American economic health so much as it is a symptom of global desperation for a predictable store of value. When the world catches fire, investors run to the only house with a functioning sprinkler system, even if the owner of that house is the one holding the matches.

Washington and Iran are locked in a cycle of escalation that provides no clear off-ramp for the international community. Diplomacy has become a performative art form while the real decisions are made through naval deployments and drone strikes. Traders who ignore the long-term implications of this shift do so at their own peril. The dollar's 10-day high is merely the opening act of a larger realignment. Expect to see a permanent geopolitical premium baked into every major asset class. Stability is the new luxury good. It will be priced accordingly.